|

Debt Awareness Week is an annual event dedicated to raising awareness about the importance of financial literacy and responsible debt management. Held each year, it serves as a reminder for individuals to take control of their finances, understand the implications of debt, and adopt healthy financial habits. This webpage aims to provide valuable insights into Debt Awareness Week and offer practical tips to enhance financial literacy.

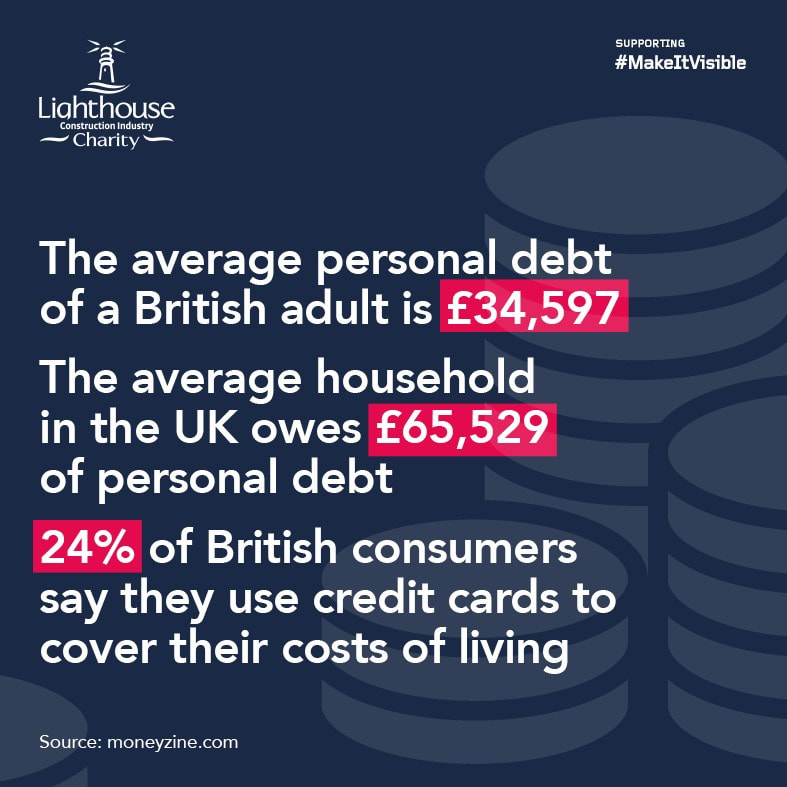

Debt is a financial obligation that arises when one borrows money from a lender with the promise of repayment, usually with interest. While debt can be a useful tool for achieving goals such as purchasing a home or investing in education, it can also become a burden if not managed wisely. Understanding the types of debt, including credit cards, loans, and mortgages, is essential for making informed financial decisions. |

|

Importance of Financial Literacy

Financial literacy refers to the knowledge and skills needed to make informed and effective financial decisions. It empowers individuals to budget effectively, save for the future, and avoid falling into debt traps. By improving financial literacy, individuals can build a strong financial foundation, protect themselves from financial hardship, and achieve their long-term goals.

Financial literacy refers to the knowledge and skills needed to make informed and effective financial decisions. It empowers individuals to budget effectively, save for the future, and avoid falling into debt traps. By improving financial literacy, individuals can build a strong financial foundation, protect themselves from financial hardship, and achieve their long-term goals.

Tips for Financial Literacy:

Budgeting: Create a monthly budget to track income and expenses. Allocate funds for essentials such as housing, utilities, and groceries, and set aside savings for emergencies and future goals.

Debt Management: Prioritise high-interest debt and develop a repayment plan to pay it off as quickly as possible. Consider consolidating debt or negotiating with creditors to lower interest rates or payment terms.

Saving and Investing: Start saving early and regularly contribute to a savings account or retirement plan. Explore investment options such as stocks, bonds, and mutual funds to grow your wealth over time.

Credit Management: Monitor your credit score regularly and understand the factors that influence it, such as payment history and credit utilisation. Use credit responsibly and avoid maxing out credit cards or opening unnecessary accounts.

Budgeting: Create a monthly budget to track income and expenses. Allocate funds for essentials such as housing, utilities, and groceries, and set aside savings for emergencies and future goals.

Debt Management: Prioritise high-interest debt and develop a repayment plan to pay it off as quickly as possible. Consider consolidating debt or negotiating with creditors to lower interest rates or payment terms.

Saving and Investing: Start saving early and regularly contribute to a savings account or retirement plan. Explore investment options such as stocks, bonds, and mutual funds to grow your wealth over time.

Credit Management: Monitor your credit score regularly and understand the factors that influence it, such as payment history and credit utilisation. Use credit responsibly and avoid maxing out credit cards or opening unnecessary accounts.